PDF Publication Title:

Text from PDF Page: 069

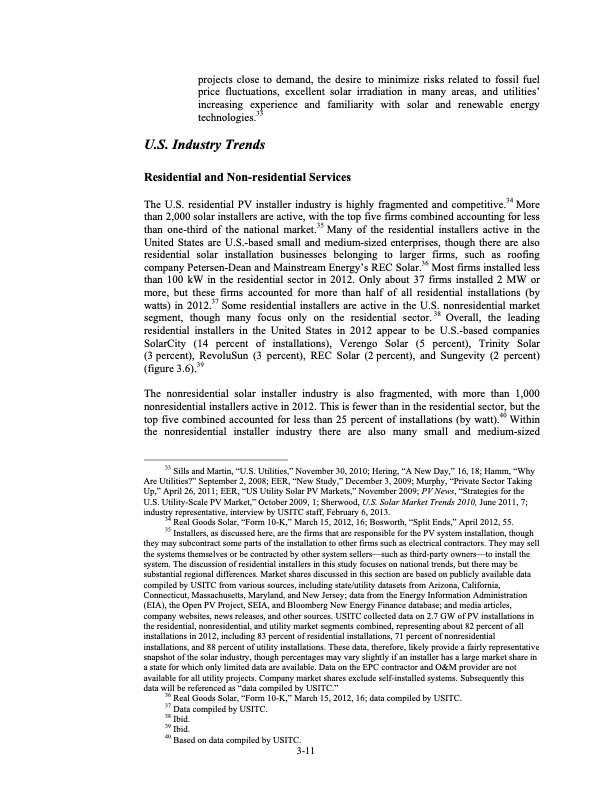

projects close to demand, the desire to minimize risks related to fossil fuel price fluctuations, excellent solar irradiation in many areas, and utilities’ increasing experience and familiarity with solar and renewable energy technologies.33 U.S. Industry Trends Residential and Non-residential Services The U.S. residential PV installer industry is highly fragmented and competitive.34 More than 2,000 solar installers are active, with the top five firms combined accounting for less than one-third of the national market.35 Many of the residential installers active in the United States are U.S.-based small and medium-sized enterprises, though there are also residential solar installation businesses belonging to larger firms, such as roofing company Petersen-Dean and Mainstream Energy’s REC Solar.36 Most firms installed less than 100 kW in the residential sector in 2012. Only about 37 firms installed 2 MW or more, but these firms accounted for more than half of all residential installations (by watts) in 2012.37 Some residential installers are active in the U.S. nonresidential market segment, though many focus only on the residential sector.38 Overall, the leading residential installers in the United States in 2012 appear to be U.S.-based companies SolarCity (14 percent of installations), Verengo Solar (5 percent), Trinity Solar (3 percent), RevoluSun (3 percent), REC Solar (2 percent), and Sungevity (2 percent) (figure 3.6).39 The nonresidential solar installer industry is also fragmented, with more than 1,000 nonresidential installers active in 2012. This is fewer than in the residential sector, but the top five combined accounted for less than 25 percent of installations (by watt).40 Within the nonresidential installer industry there are also many small and medium-sized 33 Sills and Martin, “U.S. Utilities,” November 30, 2010; Hering, “A New Day,” 16, 18; Hamm, “Why Are Utilities?” September 2, 2008; EER, “New Study,” December 3, 2009; Murphy, “Private Sector Taking Up,” April 26, 2011; EER, “US Utility Solar PV Markets,” November 2009; PV News, “Strategies for the U.S. Utility-Scale PV Market,” October 2009, 1; Sherwood, U.S. Solar Market Trends 2010, June 2011, 7; industry representative, interview by USITC staff, February 6, 2013. 34 Real Goods Solar, “Form 10-K,” March 15, 2012, 16; Bosworth, “Split Ends,” April 2012, 55. 35 Installers, as discussed here, are the firms that are responsible for the PV system installation, though they may subcontract some parts of the installation to other firms such as electrical contractors. They may sell the systems themselves or be contracted by other system sellers—such as third-party owners—to install the system. The discussion of residential installers in this study focuses on national trends, but there may be substantial regional differences. Market shares discussed in this section are based on publicly available data compiled by USITC from various sources, including state/utility datasets from Arizona, California, Connecticut, Massachusetts, Maryland, and New Jersey; data from the Energy Information Administration (EIA), the Open PV Project, SEIA, and Bloomberg New Energy Finance database; and media articles, company websites, news releases, and other sources. USITC collected data on 2.7 GW of PV installations in the residential, nonresidential, and utility market segments combined, representing about 82 percent of all installations in 2012, including 83 percent of residential installations, 71 percent of nonresidential installations, and 88 percent of utility installations. These data, therefore, likely provide a fairly representative snapshot of the solar industry, though percentages may vary slightly if an installer has a large market share in a state for which only limited data are available. Data on the EPC contractor and O&M provider are not available for all utility projects. Company market shares exclude self-installed systems. Subsequently this data will be referenced as “data compiled by USITC.” 36 Real Goods Solar, “Form 10-K,” March 15, 2012, 16; data compiled by USITC. 37 Data compiled by USITC. 38 Ibid. 39 Ibid. 40 Based on data compiled by USITC. 3-11PDF Image | Renewable Energy and Related Services: Recent Developments

PDF Search Title:

Renewable Energy and Related Services: Recent DevelopmentsOriginal File Name Searched:

pub4421.pdfDIY PDF Search: Google It | Yahoo | Bing

NFT (Non Fungible Token): Buy our tech, design, development or system NFT and become part of our tech NFT network... More Info

IT XR Project Redstone NFT Available for Sale: NFT for high tech turbine design with one part 3D printed counter-rotating energy turbine. Be part of the future with this NFT. Can be bought and sold but only one design NFT exists. Royalties go to the developer (Infinity) to keep enhancing design and applications... More Info

Infinity Turbine IT XR Project Redstone Design: NFT for sale... NFT for high tech turbine design with one part 3D printed counter-rotating energy turbine. Includes all rights to this turbine design, including license for Fluid Handling Block I and II for the turbine assembly and housing. The NFT includes the blueprints (cad/cam), revenue streams, and all future development of the IT XR Project Redstone... More Info

Infinity Turbine ROT Radial Outflow Turbine 24 Design and Worldwide Rights: NFT for sale... NFT for the ROT 24 energy turbine. Be part of the future with this NFT. This design can be bought and sold but only one design NFT exists. You may manufacture the unit, or get the revenues from its sale from Infinity Turbine. Royalties go to the developer (Infinity) to keep enhancing design and applications... More Info

Infinity Supercritical CO2 10 Liter Extractor Design and Worldwide Rights: The Infinity Supercritical 10L CO2 extractor is for botanical oil extraction, which is rich in terpenes and can produce shelf ready full spectrum oil. With over 5 years of development, this industry leader mature extractor machine has been sold since 2015 and is part of many profitable businesses. The process can also be used for electrowinning, e-waste recycling, and lithium battery recycling, gold mining electronic wastes, precious metals. CO2 can also be used in a reverse fuel cell with nafion to make a gas-to-liquids fuel, such as methanol, ethanol and butanol or ethylene. Supercritical CO2 has also been used for treating nafion to make it more effective catalyst. This NFT is for the purchase of worldwide rights which includes the design. More Info

NFT (Non Fungible Token): Buy our tech, design, development or system NFT and become part of our tech NFT network... More Info

Infinity Turbine Products: Special for this month, any plans are $10,000 for complete Cad/Cam blueprints. License is for one build. Try before you buy a production license. May pay by Bitcoin or other Crypto. Products Page... More Info

| CONTACT TEL: 608-238-6001 Email: greg@infinityturbine.com | RSS | AMP |